How to Buy Down Your Mortgage Rate (And When It Actually Makes Sense)

Interest rates aren’t just a headline—they directly control your monthly payment and your long-term cost of owning a home. The good news: you don’t have to accept the rate you’re given. You can buy it down.

Interest rates aren’t just a headline—they directly control your monthly payment and your long-term cost of owning a home. The good news: you don’t have to accept the rate you’re given. You can buy it down.

The smarter question isn’t can you—it’s should you.

What Does It Mean to “Buy Down” Your Rate?

A rate buydown means paying an upfront fee at closing to secure a lower interest rate on your mortgage.

- This fee is typically called “points”

- 1 point = 1% of your loan amount

- Each point typically lowers your rate by about 0.25% (varies by lender and market)

Example:

Loan amount: $400,000

1 point = $4,000

Rate reduction: ~0.25%

That lower rate = lower monthly payment for the life of the loan.

Two Main Types of Rate Buydowns

1. Permanent Buydown

You pay upfront once, and your rate is reduced for the entire loan term.

Best for:

- Buyers planning to stay in the home long-term

- Buyers who want predictable, lower monthly payments

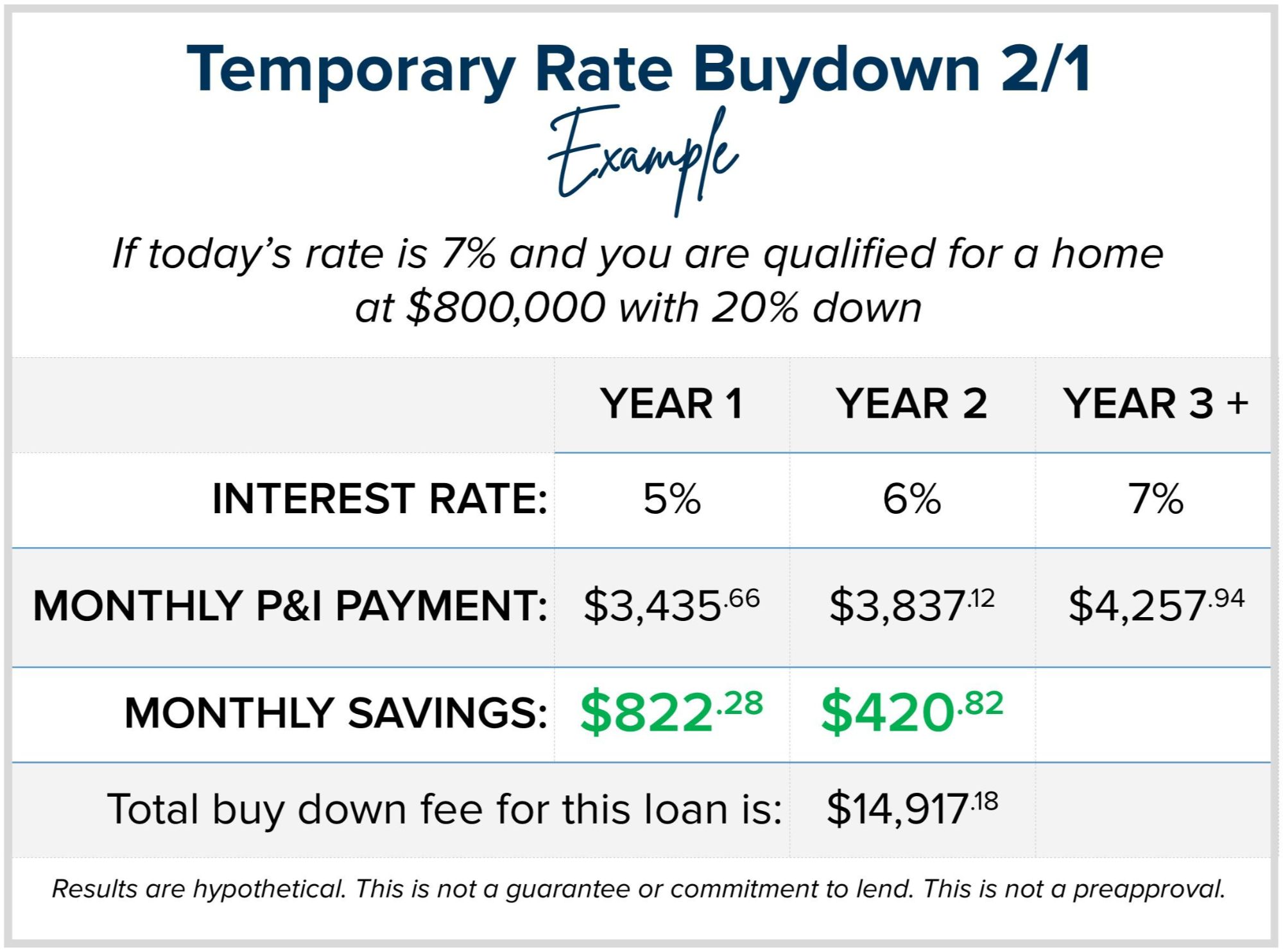

2. Temporary Buydown (2-1 or 3-2-1)

Your rate is reduced temporarily—usually for the first 1–3 years.

Example (2-1 buydown):

- Year 1: Rate is 2% lower

- Year 2: Rate is 1% lower

- Year 3+: Full rate applies

Often, the seller pays for this as a concession.

Best for:

- Buyers expecting income growth

- Buyers planning to refinance

- Buyers who want lower payments upfront

The Break-Even Rule (This Is What Matters Most)

Buying down your rate only makes sense if you stay in the home long enough to recoup the upfront cost.

Simple formula:

Cost of buydown ÷ Monthly savings = Break-even timeline

Example:

- Buydown cost: $4,000

- Monthly savings: $150

- Break-even: ~27 months

If you plan to stay longer than that → it can be worth it

If not → you’re likely losing money

When Buying Down Your Rate Makes Sense

✔ You plan to stay in the home for several years

✔ You want to lock in a lower long-term payment

✔ You have extra cash at closing

✔ The seller is offering concessions you can use toward the buydown

When It Doesn’t Make Sense

✘ You may sell or refinance soon

✘ You’re tight on cash for closing

✘ The monthly savings are minimal compared to the upfront cost

✘ You’re better off using that money to reduce your loan amount

Smart Strategy: Use Seller Concessions

In today’s market, many buyers are negotiating seller concessions.

Instead of asking for a price reduction, consider this:

👉 Use that money to buy down your rate

Why this works:

- It directly lowers your monthly payment

- It improves affordability immediately

- It can be more impactful than a small price drop

Final Thought

A lower rate isn’t always about timing the market—it’s about structuring your deal the right way.

Buying down your mortgage rate can be a powerful tool, but only if it aligns with your timeline, your cash position, and your long-term plan.

The buyers winning right now aren’t just negotiating price—they’re negotiating terms.

Categories

Recent Posts